Buying your first home is an exciting milestone, but navigating the process can be confusing for a first-time buyer. The mortgage application process especially can feel intimidating. How long does it take to get a mortgage? What do I need to apply for a mortgage? These are just some of the questions you may have as you begin your homebuying journey. We created this guide to getting a mortgage to help you better understand the process. Whether you're buying your first home in Eureka Springs, Berryville, Harrison, Cassville, or elsewhere, we are here to help you know what to expect so you can go through the mortgage process as smoothly as possible.

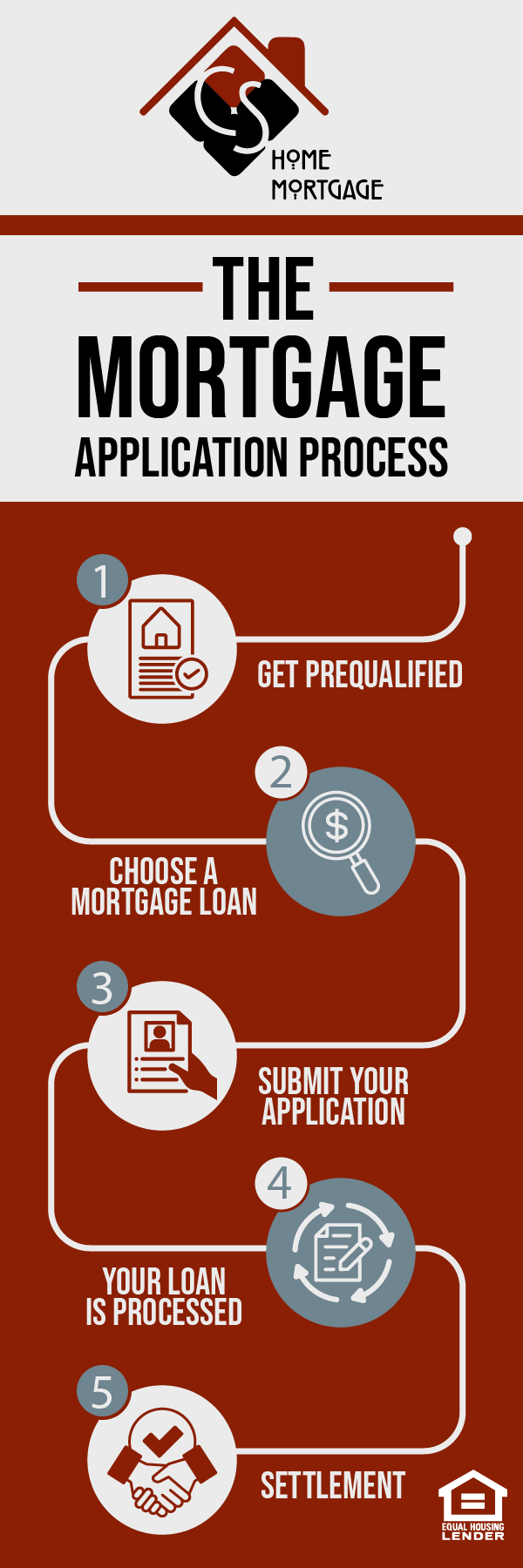

Get Prequalified For A Mortgage

When you're ready to buy a house, the first step in the mortgage application process is to get prequalified. When you get prequalified, a mortgage lender gives you a rough estimate of how much mortgage you would likely qualify for based on your self-provided financial information. To get prequalified for a mortgage, fill out a mortgage application online.

Getting prequalified should make the full mortgage process easier. If you’re planning to buy your home soon, you’ll want to start the prequalification process now. Just keep in mind that prequalification letters usually have an expiration date of one to three months from the date issued.

Once you're prequalified or pre-approved, don’t make any major changes to your finances such as applying for a new loan or credit card or drawing down your savings to make a large purchase. These changes could impact your loan approval. Learn more about what to avoid during the homebuying process with our Homebuyer Do's and Don’ts.

Choose The Best Mortgage

After you get prequalified the next step in the mortgage application process is to look at homes. If you’re having trouble finding the right house, check out our smart house hunting tips. Once you find the perfect one and have your offer accepted, it’s time to decide on a mortgage loan and complete the underwriting process. Our mortgage lenders in Northwest Arkansas and Southwest Missouri can help you find the right mortgage loan based on how much you can afford and the size of your down payment. CS Home Mortgage offers the following mortgage loans for first-time homebuyers:

- Fixed-Rate Mortgage: This is the most popular type of mortgage loan. A fixed rate means the interest rate stays the same for the entire loan term, making it a popular choice for buyers who want a predictable monthly mortgage payment and plan to stay in their homes over the long run.

- Variable-Rate Mortgage: With this type of home loan, the interest rate can change over time, according to the loan terms. Adjustable-rate mortgages often have an introductory fixed rate that is lower than average, which can be appealing when rates are high or for buyers who expect to sell or refinance before the rate increases.

- FHA Loan: Backed by the Federal Housing Administration, these mortgage loans are ideal for first-time homebuyers who want to make a lower down payment or who need more flexibility with credit scores.

- USDA Loan: Available in certain rural and suburban areas, USDA loans offer competitive interest rates and up to 100% financing. Borrowers must meet eligibility requirements.

- VA Loan: VA loans are a benefit for veterans and active-duty service members. The primary benefits of a VA loan include competitive interest rates, no down payment, and no mortgage insurance requirement.

Submit Your Mortgage Application

Once you’ve decided on a type of mortgage loan, it’s time to complete your mortgage application. If you got prequalified at the beginning of your homebuying journey, you’ve probably already submitted most of your required documentation. However, there may be some additional documents to provide or information to update.

Here’s what you’ll typically need to submit:

- Updated financial statements

- Proof of income

- Information about your assets and debts

- Details about the home you’re buying, including the sale contract

You can apply for a mortgage online through our easy-to-use platform or visit one of our branches in Northwest Arkansas or Southwest Missouri to meet with a local mortgage lender.

From submission to closing, the mortgage approval process can take an average of 30 to 45 days. You can help keep the process on track by having your documentation ready and responding quickly to any questions or requests from your lender.

Your Loan is Processed

In this step in the mortgage application process, your loan moves into the processing stage. This means your lender will verify all the information you've provided and gather any additional documentation needed. The two key steps that take place during loan processing are:

- Loan Estimate: After you submit your application, you’ll receive a Loan Estimate that shows the projected total costs associated with your mortgage, including the interest rate, monthly payment amount, and closing costs.

- Underwriting: The underwriting process consists of an in-depth review of your financial situation. Mortgage underwriters assess your ability to repay the loan based on your credit history, income, debts, and other factors.

During the loan processing stage, your lender or processor may request additional information or clarification. Be sure to respond promptly to keep the process moving along.

Close on Your New Home Loan

Closing day is an exciting milestone, the final step in your mortgage application process. This is when you sign the final paperwork, settle the closing costs, and officially become the owner of your new home.

You’ll need to bring the following to closing:

- A government-issued photo ID

- A certified or cashier’s check for closing costs (unless they are rolled into your loan)

- Proof of homeowners insurance

- Any other documents requested by your lender

Once all the documents are signed, the funds will be released to the seller, and you’ll get the keys to your new home. Congratulations, your dream of homeownership is now a reality!

Other Steps in the Homebuying Process

Last but not least, you should keep in mind that other steps in the homebuying process can affect your mortgage application timeline. These usually take place between when your offer is accepted and when you close. For a more detailed explanation process, check out our First-Time Homebuyer Guide. The three steps in the homebuying process with the greatest ability to delay your application process include:

- Inspection: While optional, getting a professional home inspection done gives you peace of mind that the property is in good condition. If any issues are uncovered, you still have time to address them before closing.

- Appraisal: Your lender will conduct an appraisal of the home’s fair market value. If it’s less than the loan amount, you may have to renegotiate with the seller or bring money to closing.

- Title Search: A title search is conducted before closing to make sure there aren’t any legal claims or liens against the property.

CS Home Mortgage Is Here to help You Through The Mortgage Application Process

We are a full-service mortgage lender serving homebuyers in Northwest Arkansas and Cassville, MO. Explore our mortgage loans, use our mortgage calculator tool to determine how much you can afford, and contact our local mortgage lenders with questions or to start the pre-qualification process. Ready to start your mortgage application? You can conveniently apply online.